Private equity (PE) has found ophthalmology. Working as investment management companies, PE firms have gravitated toward ophthalmology for multiple reasons, including the demographic changes our specialty has seen recently; the imbalance of physician supply and demand, which is projected to become more pronounced; the availability of various revenue streams and cash-pay opportunities; and the increasing complexity of the ophthalmology business. Further, similar to analogous US health care markets, the ophthalmology sector has begun to consolidate. PE has emerged as a primary catalyst for this consolidation trend.

In May 2014, the first deal between a PE firm and an ophthalmology practice was announced. Varsity Healthcare Partners acquired Baltimore-based Katzen Eye Group to form EyeCare Services Partners. According to a press release announcing the partnership, the purpose of the transaction was to consolidate successful vision care practices and affiliated surgical centers.1

Since that time, many other transactions between PE firms and large, well-developed ophthalmic practices have been consummated, including the deal between H.I.G. Capital and our institution, Barnet Dulaney Perkins Eye Center.2 What made this deal unusual was the simultaneous affiliation with a large competing ophthalmic practice in our geographic region, Southwestern Eye Center.

FRIENDLY COMPETITORS

Barnet Dulaney Perkins Eye Center and Southwestern Eye Center have been friendly competitors in the Arizona market for more than 20 years. We have a history of working well together and sharing best practices. Having both practices enter into an affiliation capitalized by H.I.G. Capital, I believe, created the largest transaction in the history of the pure-play ophthalmic and optometric care space. We are currently executing a disciplined integration strategy to create significant synergies, and we are unifying a combined platform for significant growth. In the case of our transaction, PE served as a vehicle to bring together two great organizations and create a mechanism by which we now have the ability to create a large, national footprint.

We will continue to operate under the individual Barnet Dulaney Perkins and Southwestern Eye Center brands. We decided this mutually, as both practices have developed well-recognized brands over a long period, and patients have come to know and trust these brands independently. With that said, we will take advantage of meaningful synergies in areas including revenue cycle management, finance, purchasing, infrastructure, and marketing and standardization of compliance.

WHAT GOES INTO THE DECISION?

Several years ago, through a series of internal meetings with Barnet Dulaney Perkins Eye Center executives and shareholders, we determined that the best strategy for our practice was to partner with a PE firm to accelerate growth and provide shareholder liquidity. After researching the PE landscape, one concept that I learned in that process was that, like the stock market, PE firms come in all shapes and sizes, all with different philosophies, strategies, and risk profiles. I also learned that the biggest consideration in deciding what firm to partner with is rooted in the individuals who will represent the PE team—the principals with whom your own practice will be working, first to put the deal together and, ultimately, to develop a strategy and work together at the board of directors level.

After meeting with a few PE firms, H.I.G. Capital stood at the front of the pack. Along with a core group of partners of the practice, I spent about 9 months developing a great relationship with several of the principals at the firm. Our motive for partnering with H.I.G. Capital hinged on three key considerations.

H.I.G. has an excellent track record, particularly in the health care space. Although many PE firms are interested in health care now, not all deal specifically with provider health care service businesses like ophthalmology. This important difference was significant to us in selecting the appropriate PE firm. We felt that H.I.G. Capital had the requisite expertise, growth orientation, and genuine interest in a partnership with management and the physician owners.

In addition to finances, H.I.G. brought other resources to the table. Another important aspect in choosing the right PE partner was the firm’s ability to bring assets besides money to the table, such as integration, best practices, call centers, and procurement. Every PE firm has money; what separated H.I.G. from the pack was its ability to bring these other resources to the platform that we are working so hard to develop.

H.I.G. had the certainty of closing a transaction. Although all PE firms seem to be interested in ophthalmology now, only a select few have actually closed a transaction in the space. There is a lot of work that goes into getting ready for a transaction and the preceding due diligence. This period takes the management team away from running the business on a full-time basis, and therefore taking this risk makes sense only if the team is certain that the PE partner can close a transaction in the space. H.I.G. Capital is now the only PE firm nationally to have closed two significant transactions in the ophthalmology industry in the same market. Given the investment of time and energy required to complete a transaction, confidence in the firm you choose is crucial, as failure to close a transaction can have significant negative repercussions for a business in terms of financial performance, team morale, and the effort required to identify an alternative partner.

NEGOTIATIONS

Once we got to a point where the partners and executives at Barnet Dulaney Perkins Eye Center felt ready to make a deal with H.I.G. Capital, we negotiated a letter of intent. The next step was to execute legal documents, including the purchase and sale agreement, shareholder agreement, employment agreements, and other supporting documentation. The final transactions for Barnet Dulaney Perkins Eye Center and Southwestern Eye Center closed almost simultaneously in March 2017.

I think the biggest takeaway regarding what goes into choosing a PE firm is that significant time must be spent getting to know the key people involved in the PE firm, understanding the firm’s philosophy and strategy, and developing relationships between the deal team and the doctors and management team before initiating a letter of intent.

THOUGHTS ON CONSOLIDATION

The current health care environment continues to become increasingly complex, and scale is important. In addition to the nuances of operating health care practices and overcoming governmental hurdles, such as the US Medicare Access and CHIP Reauthorization Act, physicians must continue to incorporate new technologies and treat the growing demographic of aging baby boomers—all with a diminishing pool of available providers.

Not only is consolidation a thoughtful, organized way to take eye care providers down the road to success in navigating health care and its never-ending requirements and reimbursement issues, but it is also a strategic means of bridging the gap between the decreasing number of practicing eye care specialists and the increasing number of patients. I believe the consolidation of ophthalmology practices can help us to meet the demands of the public and to provide them with the best technologies available.

As one form of consolidation, PE offers resources in capital and brings practices together. PE can serve as a mechanism for improving efficiencies, meeting patient demands, and encouraging more professional business development and structure. These improvements to our businesses will make the practice of ophthalmology more sustainable.

PE also creates an opportunity for smaller practices to join in the consolidation movement, and I think this concept is often overlooked. It is important to understand that there is plenty of room in ophthalmology for all types of eye care platforms, including those that are financed by PE and those that are independently owned. I do not believe that independently owned practices will be squeezed out of ophthalmology because of consolidation or because of PE transactions.

FOCUS ON PATIENT CARE

The most important aspect of eye care is the practice of medicine, and PE firms typically allow the management teams and doctors to manage patient care, which is squarely within our area of expertise. The right PE firm—and I emphasize the word right—provides the practice with a platform characterized by a solid infrastructure for the delivery of optimal patient care.

Right now, I believe that demand is outpacing the industry’s ability to deliver care and that we are rendering a significant percentage of the population unserved. The resources of certain PE firms can enable us to tap into that market and deliver better care to more patients. That, in a nutshell, is why Barnet Dulaney Perkins picked H.I.G. Capital from among the list of leading PE firms.

FINAL THOUGHTS

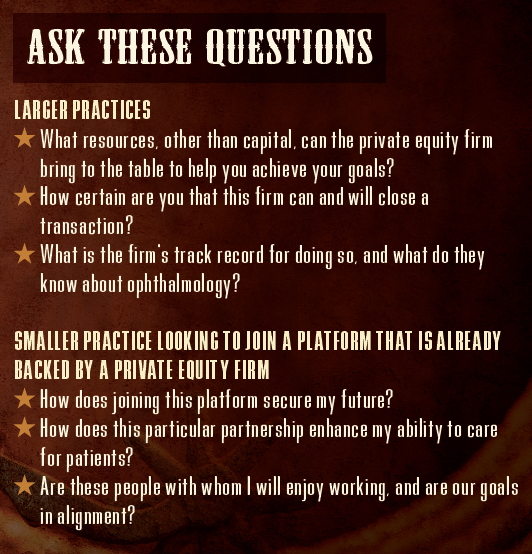

To any ophthalmology practice considering a PE partnership, I would recommend exercising careful consideration. A PE partnership is like a marriage in many ways. Right now, many owners are looking at the money that PE represents and the potential valuation of their practices. I would caution against focusing on that short-term gain and recommend carefully and circumspectly evaluating the strategy behind the decision. Regardless of whether yours is a larger or smaller practice, ask questions, including those in the sidebar on this page.

You can negotiate anything in a transaction, whether it be between two practices, two doctors, or a practice and a PE firm. What the success of a transaction really boils down to is the relationships among the people sitting around the table making the deal. I think that these relationships are the most important area of focus.

1. Varsity Healthcare Partners acquires Katzen Eye Group and together forms EyeCare Services Partners. http://www.businesswire.com/news/home/20140512005354/en/Varsity-Healthcare-Partners-Acquires-Katzen-Eye-Group. Accessed July 20, 2017.

2. H.I.G. Capital makes a strategic investment in Barnet Dulaney Perkins and Southwestern Eye Center. http://eyewiretoday.com/2017/04/19/hig-capital-makes-a-strategic-investment-in-barnet-dulaney-perkins-and-southwestern-eye-center. Accessed July 20, 2017.