Private equity (PE) firms are showing increasing interest in investing in specialty physician groups. Dentistry and dermatology were among the first to attract the attention of PE and other investors, but more recently that attention has turned to ophthalmology and orthopedics.1,2 The reason investment firms are interested in buying into ophthalmology and other medical specialty practices is rudimentary: They expect from these high-growth niche health care markets led by physicians practicing routine medicine a return on investment that is greater than they can find in other more risk-laden areas.

AT A GLANCE

- The aim of the private equity arrangement is to increase the value of the practice sufficiently so that all parties benefit upon the exit of the private equity investor.

- Private equity firms invest more than money. They invest their expertise and experience and bring a broader perspective to the practice.

So is a PE buy-in right for your practice? In this article, we explain how PE investment in a medical practice works, and we examine how to weigh the pluses and minuses for your own practice. In brief, the chief potential benefits for ophthalmologists are an infusion of cash up front, a helping hand in guiding and managing their practices efficiently, and the hope of increased value in their practices over time. Among the tradeoffs are that the ophthalmologist is no longer fully his or her own boss and that there is the potential risk of a loss when the investment partner makes its exit after the period of investment.

WHAT IS PE INVESTMENT?

(Editor’s note: In the following discussion, the abbreviation PE refers to both the activity of private equity investment and the private equity investor.) PE is a form of financing with the aim of creating value in an entity—in our discussion, an ophthalmology practice—that has great potential but limited means of investing in itself. A practice might call on PE when it wishes to expand or grow but cannot obtain sufficient financing from a bank to do so or if one shareholder in a practice wants to sell his or her shares as part of an exit strategy. In this case, a partial buyout is an option.

The PE injects capital into practices that it believes have the potential for value creation. The investment allows the practice to grow more rapidly than it would otherwise be able to (eg, to boost internationalization, to extend the products or services portfolio, or to take over another practice). Additionally, the PE may give advice on how to run the practice more efficiently. In return, the PE becomes a shareholder—generally a minority shareholder—in the practice. The growth of the practice as a result of the investment causes the value of the company—and, as a result, the shares held by both the PE and the original owners of the practice—to increase. When the value of the practice has become great enough, the PE will look to sell its shares, in order to receive compensation for the initial investment. This exit can be handled in a number of ways: for example, by sale of the PE’s shares to another investor or to the original owners of the practice.

The aim of the PE arrangement is to increase the value of the practice sufficiently so that all parties benefit upon the exit of the PE investor.

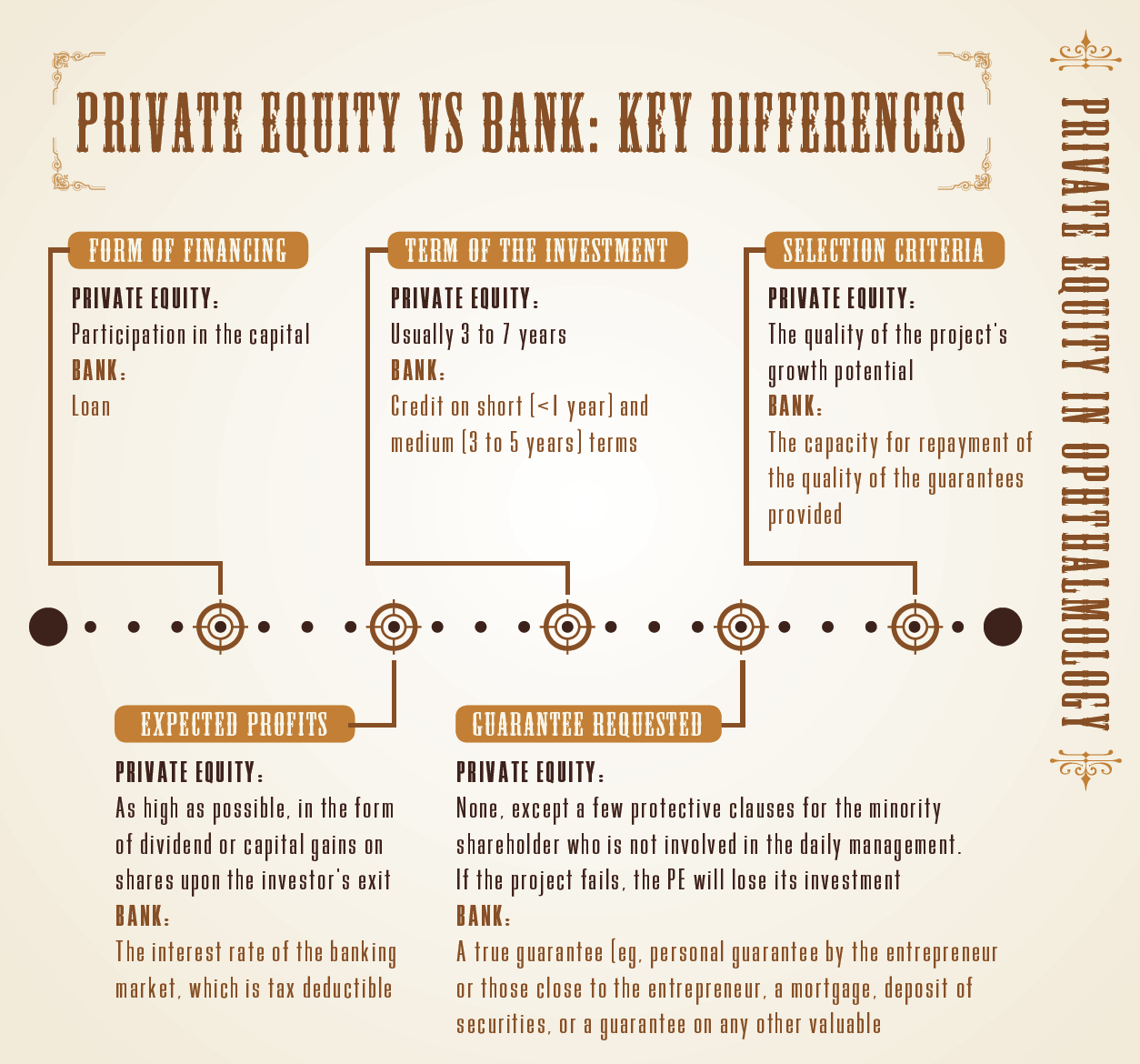

It is important to remember that PEs are not disinterested third parties, as a bank would be (see Private Equity vs Bank: Key Differences). They are partners, and generally not silent partners. They are investing in capital—the value of the practice itself—and therefore they share in losses when things go wrong. Because the PE firm is generally an expert in the development and guidance of value creation, it can offer management advice and help the practice run more efficiently. This is part of the value PE investors bring to the transaction.

HOW TO PREPARE

If you are interested in attracting PE to your practice, you must take the initiative. PE firms will not come knocking; You must go to them. You need to first identify potential investors (if possible, more than one) that are interested in medical specialty practices in general and ophthalmology specifically and that are targeting the investment amount that you are seeking. Second, you should identify which of them is right for you. Make sure the investors share your vision for how to create value in your practice. In this process, you may wish to consult with colleagues who have recently received a PE investment, or you may benefit from attending workshops or other forums where PEs are present.

Once you have identified one or more potential investors, you must devise a complete and solid business plan. This document forms the core of your presentation to the investors. Before you get the chance to present it, however, you also need to take part in some introductory steps, each of which requires its own preparation.

The elevator pitch. Suppose you had 1 minute on an elevator to present your idea to a potential investor. What would you say, and how would you say it? This type of brief introduction is obligatory for entrepreneurs who wish to present an idea to a potential investor. As the saying goes, you never get a second chance to make a first impression. Your elevator pitch should describe the essential outlines of the proposed arrangement: what your practice does, the market potential for your proposition, and the amount of funding and type of financing you are seeking. Keeping your time to under 1 minute, describe in concrete terms what you are seeking to do and how the PE can help you do it.

The first presentation. Your first formal meeting with the PE should be scheduled for an hour, though it may not last that long. It is impossible to say everything at once in such a short time, so you must be selective and remember that this is potentially only a first contact that will be followed by an ongoing dialogue between you and the investor.

You should prepare a presentation with at most 10 slides, with perhaps a few backup slides in case the investor asks a specific question. Each slide should have one main core message, including the practice’s mission statement and vision, the practice’s current leadership team, the market potential for the proposed differentiating value proposition or why you are unique, an overview of your competition, the business model or how you will sustainably generate a contribution from your winning value proposition, and the funding being sought. Even though you schedule an hour for the meeting, keep your presentation to 15 to 20 minutes to allow time for questions and discussion.

The business plan. The business plan is the central document that will serve as a basis for dialogue between the practice leadership and the investor. It should be a substantial, professional-looking document describing the opportunity for value creation that you are asking your investor to participate in. It should describe the way your management team will carry out the vision within the specified period of the PE arrangement—often a period of 3 to 5 years. It concludes with the presentation of a financial plan.

The business plan fulfills many functions. It serves as an analytical tool, listing the critical assumptions that may influence the success of the company—the team, the value proposition and its market, and the competition. It is an operational aid, concretely demonstrating how everything will be organized and laying out milestones for success. It is also a financial tool, containing a forecast of financial performance and the need for capital infusion.

There is no single perfect business plan, but a good one should contain some of the following:

- A first-class team worthy of the investor’s trust;

- A market position that offers a sustainable competitive advantage and meets a genuine need;

- A concrete demonstration of the feasibility of the proposed project (also known as proof of concept);

- A market study that indicates room for growth;

- A strong focus on a clearly identified first market; know who is your first customer, (eg, a laser eye surgery or a sports medicine patient);

- An ambitious but realistic vision;

- A roadmap with clear milestones indicating when critical assumptions made can be checked;

- A realistic risk analysis and a Plan B;

- A financial plan based on a limited number of well-supported hypotheses;

- An exit strategy for PE determined in advance; and

- Common sense and simplicity in the execution of the plans.

The data room. In addition to these elements, the practice should also prepare a virtual data room with a number of important documents regarding the practice. These should include, if applicable, the practice’s articles of association, the register of shares and shareholder agreements, minutes of board meetings, financial statements of at least the past 5 years, documentation on the competition, patent and registered trademarks, methods developed or described by the physicians of the practice, contracts with other partners or clients, employment contracts, key partnership contracts, documents showing government grants, other sources of support such as credit or financing, the curricula vitae of the physicians, and the job descriptions of key employees.

NEGOTIATING THE TERM SHEET

The agreement that binds the practice and the PE together is known as the term sheet. As part of the PE’s investment in the practice and participation as a shareholder, many changes will take place, and the term sheet serves to document and clarify all of these arrangements. It covers fundamental questions about the collaboration, including: What are the conditions for financing the investment? How will the practice be directed? What agreements must be made with the principals of the practice? How will the investor’s exit be accomplished?

Negotiations over the term sheet can be delicate because sometimes emotional issues must be addressed. Part of the planning process includes looking at worst-case scenarios and anticipating problems or crises.

A good agreement should be simple, concise, fair to all involved, and based on trust rather than on legal procedures (although these are nonetheless necessary). The agreement should still be applicable even if the practice goes through a difficult period. These are general principles, but keeping them in mind helps to keep negotiations on track.

Points covered in the term sheet include the structure of the investment; the privileges granted to the investor; the composition and role of the board of directors; remuneration for the shareholders; terms for departure of a shareholder, whether amicable or not; share options for employees who are not shareholders; confidentiality and noncompetition terms; rules for the purchase and sale of shares; and how disputes will be settled, generally through arbitration.

VALUATION OF THE PRACTICE

In order for the PE to buy into the practice, the value of the practice must be determined. The PE is buying a share in the practice, so the value of that share must be agreed upon.

There are many ways to do this. In general, the problem is that, on the one hand, the existing financial situation of the practice is not a reflection of its future potential, and on the other, the realization of that future potential is highly speculative. If the company is valued based on its current state, that will be a different number from the potential value in 3 or 5 years, after the business plan negotiated with the PE has been executed.

There are several frequently used methods for valuation, each of which has caveats. In many cases, the valuation will be calculated using multiple methods, and then the results will be combined in order to arrive at a final estimation of the enterprise value.

COLLABORATING WITH THE PE

The relationship between the practice and the PE does not stop with the investment. Most PEs spend time observing the management of the practice and providing support in order to ensure its development. Their involvement tends to be hands-on, and they act as genuine partners.

The assistance provided by the PE is usually strategic and financial, rather than affecting the daily operations of running the company, which remains the responsibility of the management. The PE almost always has a seat on the board of directors and remains in close contact with the principals of the practice. The PE provides help with corporate governance and with drawing up budgets and ensuring that they are followed.

The expertise of PEs can also be useful in establishing relationships, for example when seeking to take over or merge with another practice, and developing synergies with other parties, particularly others in their investment portfolio. With the benefit of distance, they can provide second opinions and objective advice on strategic decisions.

In other words, PEs invest more than money. They invest their expertise and experience and bring a broader perspective to the practice.

THE EXIT

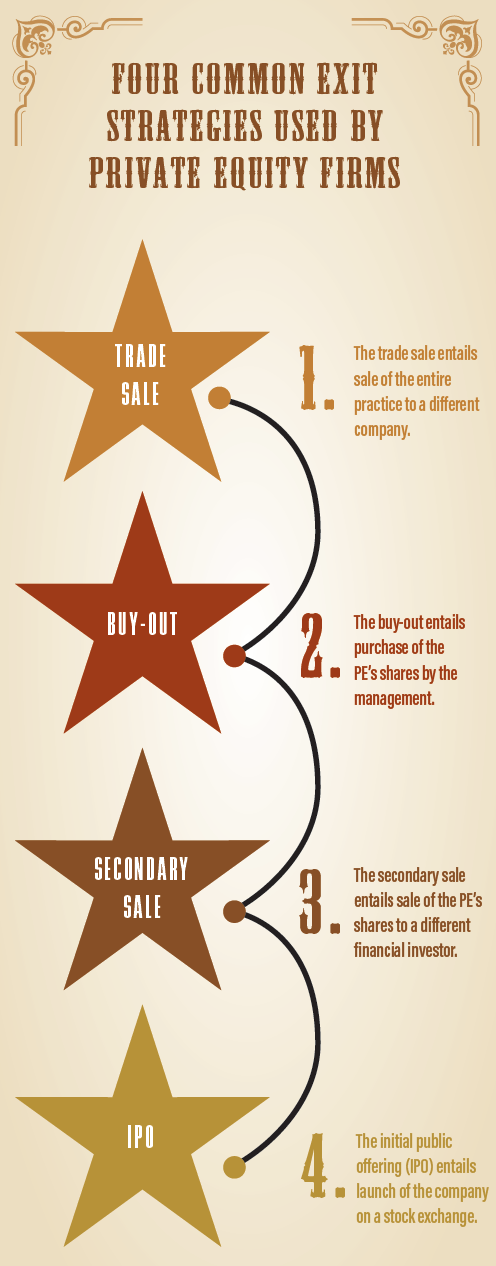

There are generally four methods by which PEs achieve their exit from an investment arrangement: trade sale, buy-out, secondary sale, and initial public offering. For a description of each, see Four Common Exit Strategies Used by Private Equity Firms.

Some of these methods are more commonly used when PEs invest in startups or early-stage companies. Because many PE investments in medical practices are in their early stages, it mostly remains to be seen how these exits will be handled.

Indications are that this trend of PE investment in medicine and ophthalmology will continue to grow. It is to be hoped that, in the end, all parties will benefit from this method of capital infusion—not only the PE investors and the physicians of these practices, but also, and equally important, the patients served by the practices.

1. Harbin TS. Private equity buyouts of ophthalmology practices. American Academy of Ophthalmology. June 7, 2017. https://www.aao.org/senior-ophthalmologists/scope/article/private-equity-buyouts-of-ophthalmology-practices. Accessed September 5, 2017.

2. Krause P. Why PE firms are buying orthopedic and ophthalmology practices. PE Hub Network. August 3, 2017. https://www.pehub.com/2017/08/why-pe-firms-are-buying-orthopedic-and-ophthalmology-practices/. Accessed September 5, 2017.