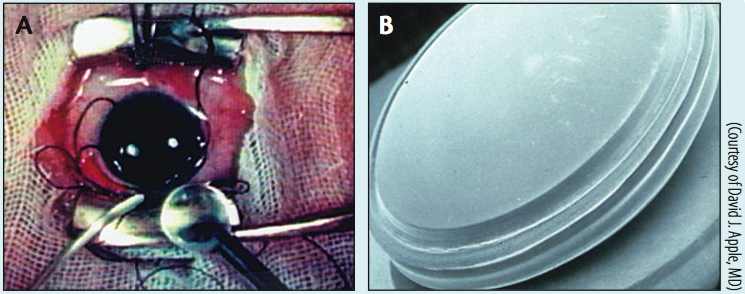

Figure 1. Sir Harold’s cinematographer filmed an IOL operation in May 1951 (A). In this image, Sir Harold has grasped the IOL for insertion into the open wound, immediately after removing the cataract. The IOL was a round, plastic disc (B).

Figure 2. Queen Elizabeth II conferred a belated Knighthood upon Sir Harold in 2000.

CRST Europe: Rayner has a big year planned in 2016, following a big one in 2015. You have launched a new OVD after the purchase of the Ophteis product range last year (Figure 3), opened a new facility (Figure 4), and have a major IOL rebranding planned. Can you help put all of these changes in perspective for our readers?

Tim Clover: Rayner is more than 100 years old. It was originally formed by two gentlemen who were optometrists. At its conception, the business was a chain of optometry practices. Over the course of 100 years, this built up to about 140 of these practices. In 1949, Harold Ridley approached Rayner and its optical specialist John Pike to make an IOL. It was a crazy idea: to put a lens into someone’s eye. That is the history of the company. After that, the IOL business grew in parallel with the optometry business.

Figure 3. Ophteis FR Pro is the first OVD with sorbitol.

I joined the company in 2014 as a non-executive director, and it was clear at that time that the optometry retail business was struggling. That is a business where scale and efficiencies are needed, and the company was not geared for that. Looking at the overall company, the optical business was a burden: lots of employees, lots of properties, a complicated business, and making little money. On the other hand, the IOL portion of the company was a great business, but it had little in terms of research and development (R&D). All the focus had been on manufacturing quality, which had stood the company well, but it is clear that a lot has happened in IOLs in the past 5 to 10 years. The company needed to either reinvent itself or possibly wither away.

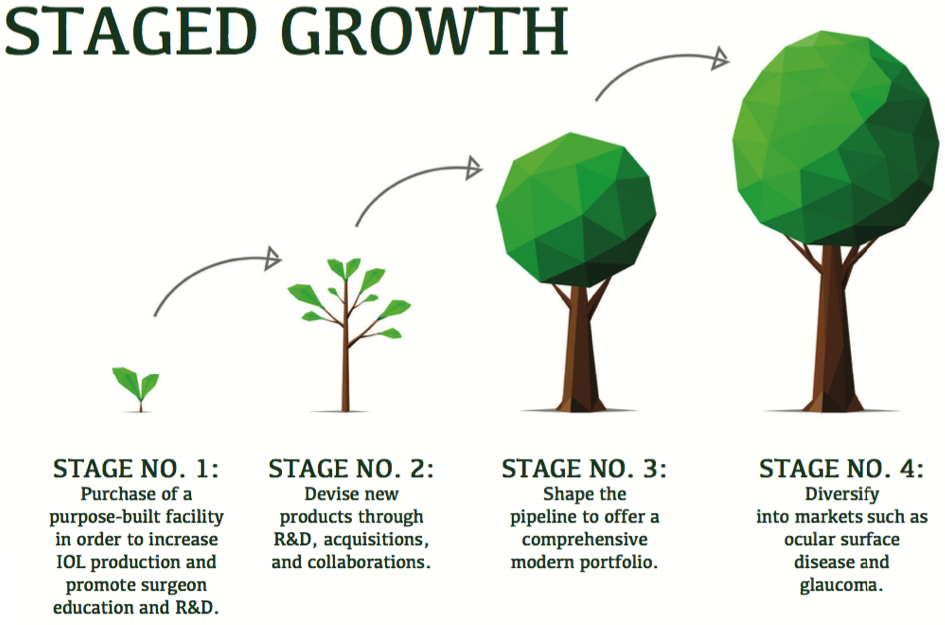

Last year, we sold all the optometry practices, and now we are focused exclusively on ophthalmology. I put together a plan for where we needed to invest and effectively embellish the product pipeline and how we are going to do that. That is what we are in the midst of executing now (see Staged Growth).

Figure 4. The Ridley Innovation Centre, Rayner’s new facility.

Our old factory made, at maximum capacity, about 800,000 IOLs a year. Last year, we sold just over 700,000 lenses. And, although it is fine to talk about expansion, we could not make any more lenses with our existing facility. Therefore, stage 1 of our plan was to buy a purpose-built facility in the United Kingdom. You are talking to me in the new center. We invested US$40 million in this center, which can now manufacture up to 3 million lenses per year. We also made sure it had great R&D and training facilities. We have a wet lab, libraries, and everything else we could think of to future-proof the facility and make it oriented toward surgeon education and R&D.

CRST Europe: Are there plans to embellish the product line?

Mr. Clover: We are working in three ways to devise new products. First is through internal R&D. Second is through acquisitions, which is what we did with the OVD line. The third and final mode of expansion is through collaborations.

This latter is where Rayner has advantages over other companies. I have been in ophthalmology for a number of years now, and one gets a sense of the shape of the market. There are the big multinational companies—the ones Market Scope calls tier 1 companies—that are driven by either internal R&D or big acquisitions. With companies of that size, an acquisition has to add hundreds of millions if not billions of dollars, euros, or pounds to make any difference whatsoever to the bottom line. Then there is another group, of which Rayner is probably at the top, of predominantly family- or founder-owned companies, with probably less than €100 million turnover.

Ophthalmology is an interesting area because there is so much innovation and so many great ideas, driven primarily by ophthalmologists but also university researchers. Who is going to take those ideas and commercialize them? It will be this second group of small- to medium-sized companies. We are one of the few private companies with a diverse shareholder base and professional management. We are at a scale where we can do a good job of commercializing those technologies, but not too big that we would be turning away 90% because they are too small for us.

So this third area of collaborative venture is where I would love to see Rayner working with the profession and with academic organizations, bringing some of these products to market.

CRST Europe: Can you be more specific about any upcoming developments?

Mr. Clover: I think anybody could look at our portfolio and say, “You could do with something more exciting in multifocality, and something around hydrophobic materials.” But we do not want to just bring out a standard product off the shelf. We would like to do something more interesting. I am confident in saying that both of those will be areas in which you will see activity from Rayner in the next 24 months or so.

The OVD that we launched in March, Ophteis FR Pro, is an example of the second type of product development. The product was the primary R&D asset that drove our acquisition of the Ophteis assets from Aptissen in Switzerland.

Ophteis FR Pro contains a molecule, sorbitol, that is totally new as far as use in an OVD. We have done clinical studies, which will be published—we will aim for presentation at the ESCRS meeting in September—which show substantial reduction in cell death compared with other OVD products in the market.

We have been working closely with Steve A. Arshinoff, MD, FRCSC, to design the final product and demonstrate its benefits. We are working with an external university, and the data will be published at a professional congress. That, I hope, sets the tone for future releases from this company.

CRST Europe: What can you tell us about RayOne IOLs?

Mr. Clover: We are currently at the point of validation and regulatory approvals, and when we start manufacturing here, in a short time, it will be a wholly new product. It will be leapfrogging, we hope, to the front of the pack in terms of product innovation, and that product will be called RayOne. It will be a fully preloaded lens with a single diameter, able to be inserted through a small incision. It will also feature a few other benefits that I will defer to the launch.

CRST Europe: IOLs now have so many potential attributes—multifocality, toricity, extended depth of focus. Where do you see it all going?

Mr. Clover: Ultimately, if you look long term, it is hard to imagine that IOLs will not be point-of-care delivery. Today, 3-D printers are producing organs and replacement parts. One can see a time when the biometry data goes into a 3-D printer and the lens is produced next to the patient, tailored exactly to his or her requirements.

I suspect that we are a long way from that. However, in the meantime, it is terrific for patients that there are so many technologies out there. In my previous life dealing with the delivery of ophthalmic care at Optegra, I was struck by one thing about premium IOL products. We were lucky because, with 23 hospitals under one corporate entity, we were able to do customer satisfaction surveys over a broad range of populations. The satisfaction levels that patients expressed with premium lenses were extremely high, into the 90% range. This is much higher than you would see for breast augmentation or other forms of elective surgery. So personally, I think the profession has been quite timid in the adoption of these technologies. Still today, only 7% of lens volume worldwide is in non-monofocal lenses. That has to be ripe for substantial growth.

CRST Europe: Does Rayner have any interest in developing other types of medical devices?

Mr. Clover: The classical model seems to be for large ophthalmic companies to offer large capital equipment—lasers, phacoemulsifiers—and to use IOLs as a sort of currency for acquiring these large machines. Rayner does not have competence in designing, maintaining, and servicing capital equipment. So, no, we have no interest at all in capital equipment. Good luck to the guys who do. Companies take huge bets on these technologies that they develop, and, if they do not pay off, they are really in trouble. I do not want any part of that.

I think it is a zero-sum game. The IOL is arguably the most important piece of the puzzle because it is the bit that stays in the eye and delivers the vision at the end of the day. I am not sure bundling is at all good for the industry; forcing practitioners to use a lens because it is a way of paying for capital equipment does not seem like a place we should be.

I like the idea of partnering. There are many great independent companies out there that offer good products, and we will be happy to work with them.

In terms of diversification, my belief is that areas like ocular surface disease present big opportunities, with a strong demographic and lifestyle drivers. I would like to see Rayner finding the right opportunity to enter markets like that and glaucoma as well, although one wonders if we have missed the boat with the microinvasive glaucoma surgery devices market at the moment.

Rather than taking on capital equipment manufacturing and design, it makes more sense to ask: What are our competences? Our competences are around our high-quality manufacturing, our professional training capabilities, our global infrastructure, being small enough to collaborate with entrepreneurs and academic institutions that produce innovations, and taking products to market quickly without some of the associated bureaucracy and other problems that come with scale. For the next few years, we have got our hands full getting the pipeline into shape to offer a comprehensive modern portfolio. After that, I think those are the areas we will be likely to look at.

CRST Europe: Where do you see the company 5 or 10 years down the road?

Mr. Clover: We would like to have a stronger geographic presence and maybe two or three new product ranges. I am sure if you read the mission statements of a lot of the companies in this sector, they talk about being an ophthalmology partner and providing innovative services. However, few of them would actually say, “We are going to do IOLs. We are going to try to do them better than anybody else. We are going to keep it simple, but we are going to stay at the front.”

I want Rayner to be that company. I think there is an enormous scope for R&D and technological development in IOLs, and there is a danger that the leaders in this market get distracted by all the other things they are doing. Instead, the one thing that should be the most important—the IOL—ends up being maybe the source of least innovation.

We have lots of growth to go through before we get to that head-scratching worry of “What’s next for us?” We are grateful for the opportunity to have people reading about the company and understanding where we are. Finally, I would say, to those people who are developing innovative products, that I hope Rayner is one of the top names on their list of potential partners.