The physician–chief executive officer (physician-CEO) is continually faced with decisions regarding capital allocation. Determining whether money is best invested in a new piece of equipment, staff member, or office space, for example, can be crucial to the success of one’s practice. When CEOs decide how to allocate capital, they consider how risky each investment is and estimate the expected return from each investment. Many investments may appear to be good because of a positive expected return, but investing only makes financial sense if the yield exceeds the cost of capital and of alternative investments.

AT A GLANCE

• Investing only makes financial sense if the yield exceeds the cost of capital and of alternative investments.

• In order to determine whether a particular capital outlay is wise, the physician-CEO must not only think about NPV and IRR but also a host of intangible considerations, such as risks, professional passions and preferences, and synergies with other activities.

For this article, let us consider the example of the purchase of a femtosecond laser for cataract and lens replacement surgery. Let us assume that the laser costs €500,000 and that we are using cash to pay for it. When faced with the decision of whether or not to purchase this laser, the financial tools net present value (NPV) and internal rate of return (IRR) are useful to evaluate the merit of the investment. We will consider each of these tools separately.

DEFINING TERMS

The first question to answer when considering the proposed laser purchase is: “Will the laser generate positive cash flow?”

In order to answer this question, we must estimate how much cash the laser will generate over time and then consider what the true value of that cash will be after factoring in inflation and the lost opportunity to earn interest.

The concept of the time value of money is important when considering these factors. This concept says that €1 today is worth more than the same €1 in the future. Would you rather have €500,000 now, or €500,000 in 5 years? The answer is obvious: having the money now means that you can either spend it now or invest it now. If invested at a compounded interest rate of 5%, the €500,000 you have today will grow to €814,447.31 by 10 years from now.

Inflation also affects the future value of cash. For example, if we assume 3% inflation, €500,000 today will be worth these amounts in the future:

- 1 year from now: €500,000 / (1 + 0.03) = €485,436

- 5 years from now: €500,000 / (1 + 0.03) X 5 = €431,034

- 10 years from now: €500,000 / (1 + 0.03) X 10 = €373,134

The reciprocal of this concept can be used to value future money in terms of today’s present value. In other words, if we know how much cash we will have in the future, we can express it in terms of today’s currency. Future cash flow discounted to today’s present value is called discounted cash flow (DCF). Three factors—inflation, risk, and financing costs—are combined to create the discount rate. The discount rate is applied to the projected future cash flow, and the DCF expresses that future cash flow in today’s currency.

NET PRESENT VALUE

In determining NPV, current and future revenues and costs are calculated and worked back to one number in today’s currency. In our laser example, NPV will consider the cash generated by the laser over time, apply the discount rate to the total cash flow, and express the total cash generated in terms of what that cash is worth in today’s currency. This amount can then be compared to the initial €500,000 investment to determine whether one would be better off keeping the €500,000 and not spending it on the laser.

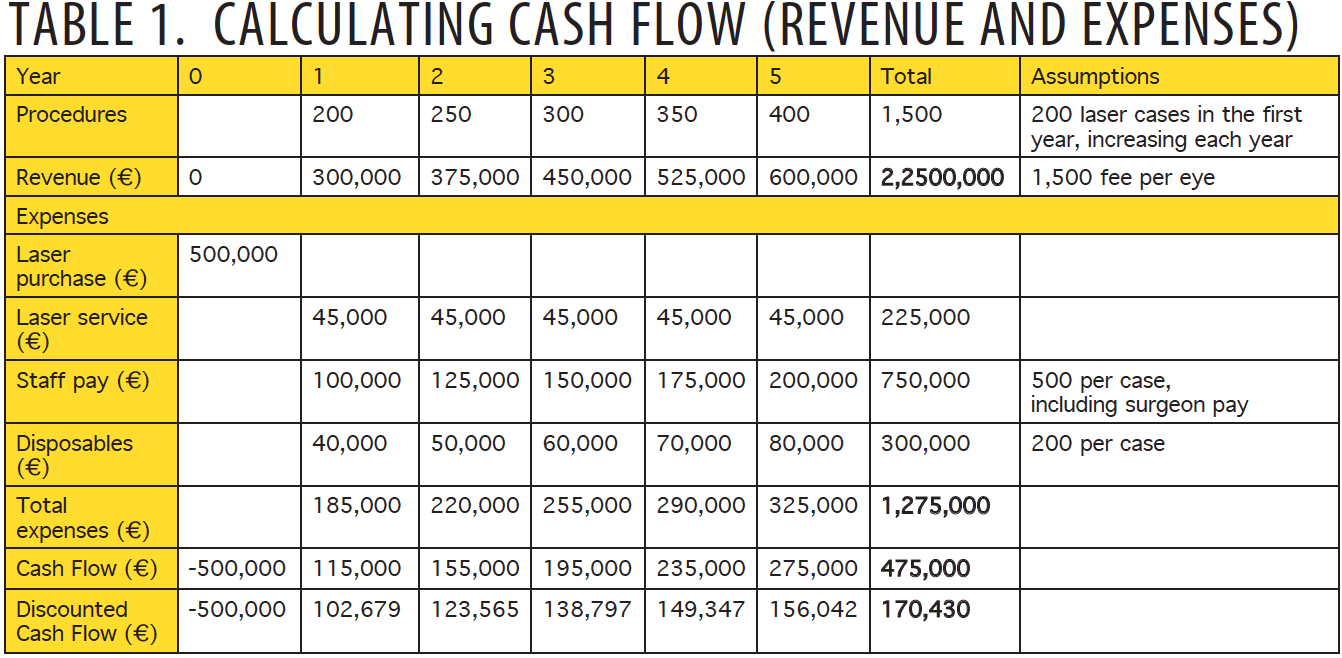

Table 1 shows projected cash flows for our example. The totals over 5 years are:

- Revenue: €2,250,000

- Expenses: €1,775,000

- Cash flow: €475,000

At first glance, the laser appears to be a good investment, as it generates €475,000. But let us take our calculations a step further to confirm whether this is still the case in today’s currency.

DISCOUNTED CASH FLOW

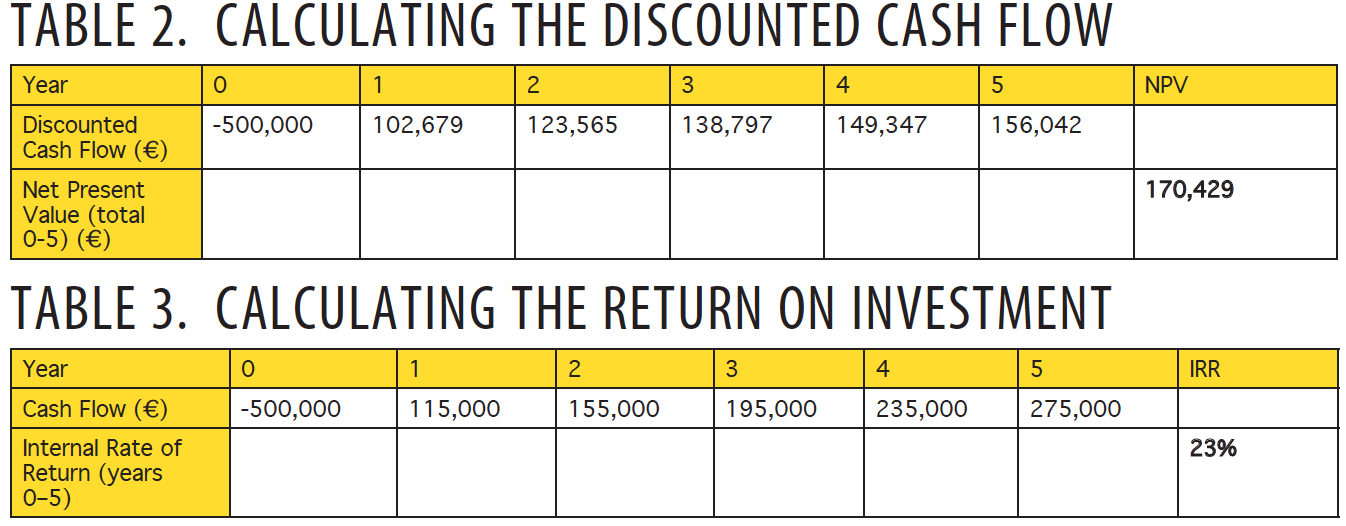

After calculating total projected cash flow, we apply the discount rate in order to determine the DCF and express the cash flow in today’s currency. In this case, we use the practice’s cost of capital (ie, average it costs the practice to finance its debt and assets) as the discount rate. For this example, we will use 12% (Table 2).

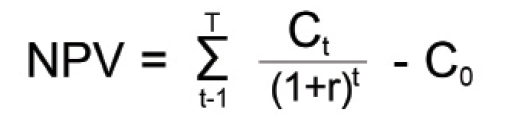

Figure 1. Net present value formula, where Ct = net cash inflow during the period t; C0 = total initial investment costs; r = discount rate; and t = number of time periods.

The formula for calculating NPV is shown in Figure 1. It may look daunting, but it can easily be calculated using built-in formulas in spreadsheet software such as Excel, Numbers, and Google Sheets.

In our laser example, the NPV is €170,429. A positive NPV means that the laser will generate a positive cash flow in today’s currency. In other words, if we purchase a laser now for €500,000, achieve the projected revenues, and stay within the projected expenses, then the laser will generate €170,429 in today’s currency. This suggests that the purchase of the laser will add value and that it may be a wise investment.

INTERNAL RATE OF RETURN

To decide whether to buy the laser now, however, we must also consider what is the return (as a percentage) on the €500,000 we are spending and whether there are other ways to spend the money that may achieve a better return. For such comparisons, we calculate the IRR, which can be used to help answer the question, “Should I purchase this laser, or am I better off using the money elsewhere, such as adding another operating room or investing the money in the stock market?”

The IRR describes the return on investment. For example, a 1-year treasury note with a 1% yield provides an IRR of 1%. A 30-year mortgage with a 5% interest rate returns an IRR of 5% to the bank. The IRR is called internal because it is isolated to the investment being considered. IRR shows the yield of the moneys invested and is based on nondiscounted cash flows.

IRR is easily calculated using a function within spreadsheet software, as shown in Table 3.

Our calculations show that the purchase of the laser results in an IRR of 23%. Because this return exceeds the cost of capital (12%), it can be considered a good investment. However, if the practice is accustomed to returns exceeding 23%, or if there is another use for the capital that may return greater than 23%, then the laser may not be the best use of capital.

CONCLUSION

The financial tools NPV and IRR are useful when determining the best use of capital. However, there are also a host of intangible considerations such as risks, professional passions or preferences, and synergies with other activities. The physician-CEO must weigh all these factors and make an informed decision.

Lance Kugler, MD

• Surgeon and CEO, Kugler Vision, Omaha, Nebraska

• Director of Refractive Surgery, University of Nebraska Medical Center

• lkugler@kuglervision.com

• Financial disclosure: None acknowledged