The prevalence of myopia is rising, and, in some parts of the world, this rise can only be described as dramatic.1 For example, in many East Asian countries, the prevalence of myopia reaches 70% or more. Further, in the United States, the prevalence of myopia has doubled during the past 30 years, and the prevalence of high myopia (greater than -8.00 D) has risen eightfold. In China, the prevalence of myopia in young adults is greater than 75%.1

Considering these worldwide demographic trends, the demand for refractive surgery can be expected to continue among our patients. But what, specifically, can be said about the prospects for the refractive surgery market in Europe? In an attempt to answer this question, I contacted a number of refractive laser and IOL manufacturers. The statistics and projections in this article are based on their estimates and on some market analysis by the well-known ophthalmic market research firm Market Scope.

At a Glance

• In all likelihood, the LVC market may continue to be

flat for the next 5 years.

• Other areas of refractive surgery, including phakic

IOLs and RLE, may experience growth for the next

5 years.

The refractive surgery market today includes laser vision correction (LVC), phakic IOLs, and refractive lens exchange (RLE) with premium IOLs. Because cataract surgery with premium IOLs can also be considered a form of refractive surgery, I also included cataract surgery in my investigation. Those results were presented in the September issue of CRST Europe (Is a Robust Growth of Premium IOLs in the Cards?, pg 42).

THE LVC MARKET

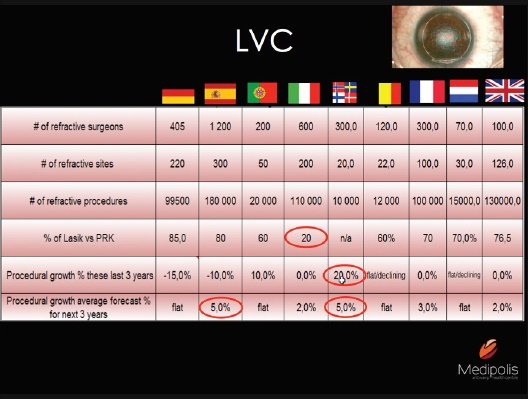

Based on the input of multiple laser manufacturers, some estimates of LVC utilization are summarized in Figure 1. If you are not well-versed in the flags of Europe, the countries listed left to right are Germany, Spain, Portugal, Italy, Scandinavia (all four countries combined), Belgium, France, Netherlands, and the United Kingdom.

In most of Western Europe, LASIK is favored over PRK as the predominant LVC procedure, accounting for 60% to 80% of total procedures. The exception is in Italy, where PRK is predominant and LASIK accounts for only 20% of LVC procedures.

Figure 1. Estimated utilization of LVC in certain European markets.

As part of my evaluation, companies were asked to describe the growth or decline in procedures, country by country, over the past 3 years. According to their input, LVC volume was flat or declining in most countries. Most notable were the dramatic decreases of 15% and 10% in Germany and Spain, respectively. By contrast, there was a 20% increase in Scandinavia; this high of an increase occurred because the numbers were low to begin with, so a small rise yielded a larger growth in percentage.

When asked to forecast LVC growth in the next 3 years, companies predicted flat or only 2% to 3% growth in most countries, the exceptions being 5% growth in both Spain and Scandinavia. In Spain, that growth can be explained by the significant decrease in LVC in the past few years as a result of the economic collapse of 2008. In Scandinavia, on the other hand, strong growth in the past 3 years is forecast to continue.

a snapshot of OTHER MARKETS

Phakic IOLs. Companies manufacturing phakic IOLs forecast double-digit growth for the next 5 years, driven by the increasing numbers of high myopes in Asia and Europe. According to Market Scope, STAAR is the predominant company in the phakic IOL market, with 68% market share, followed by Ophtec with 26%, Abbott Medical Optics with 4%, and other companies accounting for less than 2%.

Presbyopia and RLE. In the next 5 years, more than 10 million people will reach presbyopic age in Western Europe, according to Market Scope projections. The population is aging worldwide, so increasing numbers of presbyopes are entering the market. One of the best ways at present to address presbyopia surgically is through RLE with a multifocal IOL. Market Scope predicts the compound annual growth rate for RLE in Western Europe to be 4% between 2014 and 2020, with the increase driven by greater utilization of premium IOLs. About the same rate of increase is predicted for the United States.

CONCLUSION

In all likelihood, the LVC market may continue to be flat for the next 5 years. However, in other areas of refractive surgery including phakic IOLs and RLE, ophthalmologists can hope that the projections of manufacturers and market researchers cited in this article ring true in the coming years. n

1. Holden B, Sankaridurg P, Smith E, Aller T, Jong M, He M. Myopia, an underrated global challenge to vision: where the current data takes us on myopia control. Eye (Lond). 2014;28(2):142-146.

Erik L. Mertens, MD, FEBOphth

• Medical Director, Medipolis, Antwerp, Belgium

• Chief Medical Editor, CRST Europe

• e.mertens@medipolis.be

• Financial disclosure: None